All you need to know about private investments fundraising for startups and small businesses.

It is always thrilling to start a business. However, most startups lack sufficient funding for their growth. As they attempt to finalise their product or service, ramp up sales and achieve traction, it becomes more difficult for them to set aside time to private investments fundraising for their business.

To take some strain off their finances, the startup founders often rely on private investors.

So, who exactly are these private investors and how do they fund startups?

Who is a private investor?

A private investor is a person or company that puts money into a company, with the goal of helping that company succeed and getting a return on their investment.

The four main types of private investors are:

- Friends and family

Friends and family are often the first point of contact that startups turn to. They’re a great resource for pre-seed funding, as friends and family already have that base of trust that founders usually have to build from scratch with other private investors.

If you need a smaller amount of money (under €50,000 or so), this may be one of the first avenues to check out. These are the people that believe in you and want to see you succeed, so they will be less willing to cash on interest and how quickly you pay any money back. They are more likely to buy into you and your idea and need little evidence of your business succeeding.

- Angel investors

Angel investors are wealthy entrepreneurs with usually an exit in their past. They want to leverage their own wealth by investing in projects they are passionate about, especially startups at the early stages that may have difficulty accessing more traditional forms of financing. Many angel investors are successful founders themselves, as well as corporate leaders and business professionals.

They usually offer mentoring and advice alongside capital. Often angel investors pool their money with other angel investors, forming an angel syndicate.

- Venture capitalists (VCs)

Venture capitalists are people who work for venture capital firms which make bets on big opportunities like anyone would in the stock market. Unlike angel investors, they are not investing their own money, but rather the money of their employer – the VC fund. They do everything in their power to make sure their bets pay off, so they invest for the long term. Founders need to have a well-established business, a strong management team, and a good track record of success to get investment from venture capitalists.

A venture capitalist is charged with finding a relatively small number of investments (usually less than ten per year) to cover a 7 to 10 year period. While the venture capital firm may look at thousands of deals in a year, they can only pick a small amount of deals to pursue.

- Private equity (late stage VC) firms

Private equity or late stage venture capital isn’t really associated with startup capital – it’s associated with growth capital. This is a type of investment typically reserved for companies that have already grown to a larger size and are looking for a specific growth path or exit strategy that isn’t available through traditional financing.

If you’re a startup with just an idea or early product-market-fit, you’re likely too early for private equity. Typically private equity firms are looking for later-stage companies that require much larger sums of money, usually at least €5 million, in businesses that already have financial traction and some sort of assets to leverage.

How does private investments fundraising work?

Each type of private investment works differently. Here is how the four most common types of private investments fundraising work.

- Friends and family

Friends and family are a great source of early investment, but it can be a tricky relationship to navigate. It’s common for people to feel like they can be casual with these types of investors because their relationships with them are personal. That’s a mistake.

Founders should treat investment from friends and family as a professional addition to their existing personal relationship. It’s a good idea to get a written contract stipulating the terms of the investment and also to make it clear that it’s very likely they won’t get their money back. This is about setting expectations straight from the beginning. Also, you may lose the friend, if the startup fails.

- Angel investors

Angel investors are typically wealthy individuals who look to put relatively small amounts of money into startups, typically ranging from a few thousand euros to as much as a millions. They often invest at the local level, with “local” being as narrow as their own country, region or city.

Angels are often one of the more accessible forms of early-stage capital for founders and as such are a critical part of the fundraising ecosystem. Angels often look at the wider scope potentials of a startup rather than specific metrics, like for instance financials, which is what characterizes investments from VCs.

There is no definitive limit on what a single angel investor can invest, but a typical range would be from as little as €5,000 to as much as €500,000 although on average angels invest around €25,000 (at least in Finland which is where I live).

Angels may also invest incrementally, offering founders a small investment now with the opportunity to follow-on at the next round with additional investment, or invest only if some other investors are taking the lead (anchor), thus becoming minority investors.

There are three primary types of pre-seed and seed stage investments: an equity stake, a convertible note and a subordinated debt. Note that these investments are not strictly associated with angels but can also come from VCs.

Equity stake

An equity stake (or share) is when an investor exchanges their money for ownership in a startup. Equity investors often like to be involved in the decision-making process of the business. Their portion of the stake in the startup depends on the ownership size.

The amount of equity the investor receives will depend upon the company valuation that the investor and founder agreed upon. So if the founder valued the company at €1,000,000 and the investor put in €150,000 of cash, the investor would get a 15% equity stake in the company. This is something which needs to be put in what is called a shareholders agreement.

From there, equity stake can get complicated. Founders can start to issue different classes of shares, some which have voting rights or some that get paid back more quickly than others. Once again the shareholders agreement should be the source to highlight these aspects.

Convertible note

Sometimes the investor and the entrepreneur cannot agree on exactly what valuation the startup has today, because many variables are at stake i.e. financial projections, sales pipeline etc.

In that case, they may opt to issue a convertible note (also called convertible loan) that lets both parties set the value of the startup at a later stage, usually when more outside money comes in.

A convertible note is set up as a loan to the company. So if the investor put in €150,000 as a convertible note, it would mature and come due at a specific date in the future, e.g. a year from now.

During that time it will likely accrue interest. At the maturity date, the angel investor can choose to either ask to be paid back in cash or convert that money as equity into the startup based on a valuation determined at that time.

Convertible notes have become more popular with angel investors as well as founders over the years because they align both parties with the goal of maximizing the investment.

Subordinated debt

A subordinated debt is debt that is unsecured and/or ranks for interest and repayment after the senior debt of a company. In the case of default, creditors owning a subordinated debt will not be paid until the senior debt holders are paid in full.

Subordinated debt is riskier than any other type of debt. It can be any investment that’s paid after other debts and loans are repaid.

- Venture capitalists

A venture capital firm is usually run by a handful of partners who have raised a large sum of money from a group of limited partners (LPs) to invest on their behalf.

The LPs are typically large financial institutions or very wealthy individuals which are using the services of the VC to help generate big returns on their money.

The LPs have a window of 7-10 years with which to make those investments, and generate a big return. Creating a big return in such a short span of time means that VCs must invest in deals that have a big potential outcome, i.e. invest in unicorn startups.

These big outcomes not only provide great returns to the fund, they also help cover the losses of the high number of failures that high-risk investing attracts.

A small number of investments

Although VCs have large sums of money, they typically invest that capital in a relatively small number of deals. It’s not uncommon for a VC with a fund worth €100 million to manage less than 30 investments in the entire lifetime of their fund.

The reason for this is that once each investment is made, the partners must personally manage that investment for up to 10 years. While money is often plentiful, the VCs’ time is very limited.

Understandably, with such a small number of investments to make, VCs tend to be very selective in the type of deals they do, typically placing just a few capital injections per year.

Regardless, they still may see thousands of founders in a given year, making the probability of a startup being the lucky recipient of a big check pretty small.

Depending on the size of the firm, VCs will write checks as little as €250,000 and as much as €100 million. They invest both in early and later stages businesses. The most common check is around €3-5 million and is considered a “Series A” investment. It’s relatively uncommon for these checks to be the first capital into a startup. Most startups begin with finding private investors with pre-seed and seed rounds of smaller ticket sizes from friends and family, then angel investors, before turning to venture capital or other financial institutions.

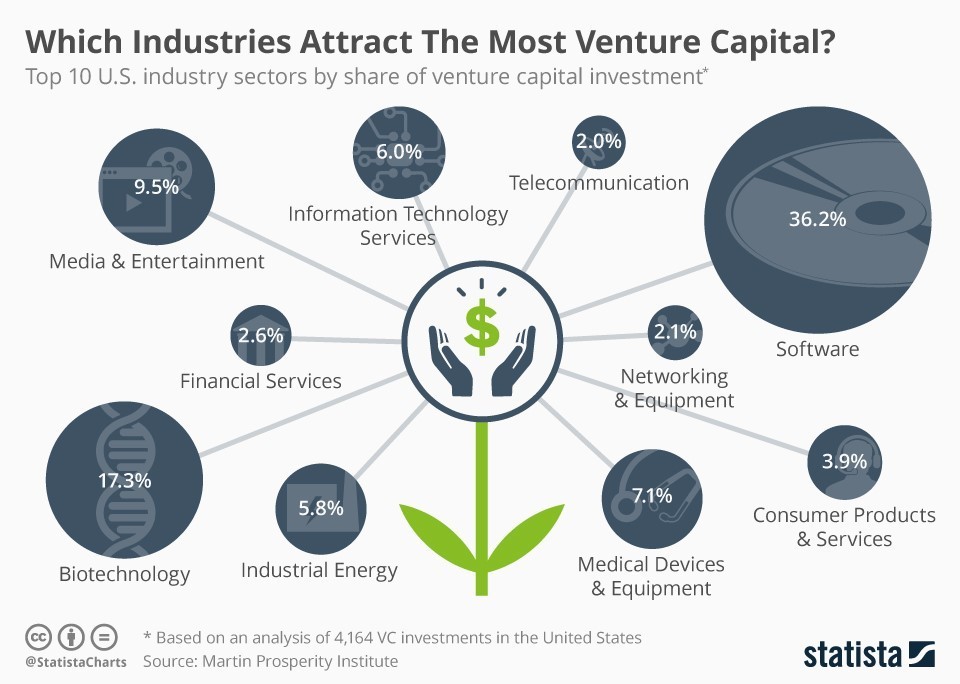

Favored industries for venture capital

Venture capitalists tend to focus on certain industries that are more likely to yield a big return. That’s why it’s common to see a lot of venture capital activity around technology companies (specifically software, SaaS and deeptech) and digital business models, as they scale faster and they could be a huge win for potential investors.

The other reason VCs tend to invest in a few industries is because that is where their domain expertise lies. When it comes to big money investing, VCs tend to go with what they know best.

VCs know that for every 20 investments they make, only one will likely be a huge win. Namely, either the startup they invested in goes public (IPO) or has enough business growth to be sold for a large amount (mergers and acquisition or simply M&A).

VCs need these big returns because the other 19 investments they make may be a total loss. The problem, of course, is that VCs have no idea which of the 20 investments will be the big thing, so they have to bet on companies that all have the potential to be the next Amazon.

VCs tend to be very selective in who they take pitches from. They have the luxury of only investing in well-prepared startups with solid business plans.

Often these relationships are based on other professionals in their network, such as angel investors who have made smaller private investments in the startups at an early stage, or founders whom they may have funded in the past.

While some VCs will in fact take pitches from an unsolicited source, it’s best bet to find an introduction through a credible source. These sources are sometimes other startups the VCs have invested into, so it’s often a good idea to check the VC portfolio on their websites and ask for a warm intro through other startups.

You can see a typical breakdown of the favored sectors for VCs in the image below.

- Private equity (late stage VC) firms

As said earlier, private equity or late stage VC is a type of investment typically reserved for later stage companies, no longer startups but scaleups.

For businesses with existing revenues or assets, private equity becomes an interesting option for business funding. Private equity is valuable to companies that have a strong operational profile, but don’t have the high return projections of a technology startup or some other trendy investment metrics like for instance exponential growth.

Private equity firms pool their money from other investors who tend to be pension funds, insurance companies, and foundations. These institutional investors invest in a private equity fund to employ a management group to seek out high yield investments on their behalf.

Unlike venture capital firms that make big early stage bets that they hope will have an enormous return when the company grows, a private equity firm bets a little less on speculative growth and a little more on demonstrated growth.

The focus is to purchase a company that they can either IPO, sell, or generate cash returns. The private equity group is essentially betting on the fact that the asset is worth more in the future than it would be worth presently. Companies funded by private equity groups usually need to exit at $1B+ (hence becoming unicorns).

There are all sorts of private equity funds, from those that do small deals at or below €5 million to those that manage multi-billion euro deals. In each case, they are looking for existing ventures that could be better scaled with outside capital.

Advantages and disadvantages of working with private investors

It’s important to acknowledge that raising capital is a difficult, time consuming and a long process that sometimes ends with no results. So before raising capital, founders should spend a good amount of time asking themselves whether they need to raise capital in the first place. If so, they should explore all types of private investments fundraising, including options like small business loans from banks or governmental grants.

Some of the advantages of private investments fundraising include:

- It is not a bank loan. In some cases private investment is an easier fundraising option than obtaining bank loans. The bank loan needs to be supported with collaterals. This is not the case in private investments. Private investors know that, if the enterprise fails, their money is lost. The business owner is not liable to return the money.

- It does not need proven credit history. Private financing is not the same as typical bank financing. It does not require any credit or demonstrated financial history. Private investors are more interested in their future earnings than what the company has done in the past.

- It gives access to investors’ expertise. Private investors are individuals who have extensive knowledge, experience, and skill in their niche. They also provide mentorship and guidance in addition to funding. Hands-on access to the high-level expertise of investors is unmatchable.

Despite the advantages of private investments fundraising, there are a few disadvantages that founders should be aware of. They are as follows:

- It dilutes the share earnings. Private investors expect ownership and a share of profit in return for their investment. As a result, an amount of startup shares are distributed to investors. A high ownership share may affect the amount of company’s margins that go to the founders.

- It affects the controlling power of the founders. Private investments have an impact on the founders’ authority. An increase in shareholders makes the founder more accountable to investors, resulting in a significant dilution of earnings and delay in the decision-making process. It also increases the chances of potential internal conflicts.

- The stakes are at higher risk. Investors demand solid outcomes from the startups in which they invest. There is constant pressure on the management team to meet the investor’s expectations. So, one must ensure that the investor’s demands are matched with the capabilities of the team.

Here are the advantages and disadvantages of private investments fundraising that a startup would likely seek.

- Friends and family

Advantages of working with friends and family

The biggest advantage of private investments fundraising from friends and family lies in the fact that a founder already has an established, trusting relationship with these people. That means they’re easier to get a meeting with, more inclined to say “yes,” and are more likely to be flexible with their expectations and timeline.

The structure of the investment will also likely be simpler than an investment from more formal investors like business angels and VCs. Founders borrowing from friends and family don’t have to fulfill complicated due diligence processes and fill out forms like they would with larger financial institutions.

Finally, raising from family and friends allow founders to keep their ownership high and remain independent.

Disadvantages of working with friends and family

There are many reasons why an entrepreneur may not want to invest with friends and family members and focus more on traditional financing options like equity financing, or even looking into small business loans.

Introducing large sums of money into a relationship that was previously entirely personal has the potential to ruin that relationship.

That’s a particularly big risk if a startup fails and investors lose all of their investment. So it’s important for founders to be very clear about the potential for loss when accepting business funding and investment money from friends and family.

Friends and family members also may not be able to add value to a company in the same way that more formal, established private investors can. VCs, for example, typically invest in startups in fields that they are familiar with. Having that kind of knowledge on board is a huge advantage for any new company looking for private funding.

Finally, the amount that founders can usually raise from family and friends might be too little to sustain a longer run. Growth will need to focus on reinvesting profits or looking for other sources of financing fairly soon.

- Angel investors

Advantages of working with angel investors

One big advantage of private investments fundraising from angel investors is that they are often more willing to take a risk than traditional financial institutions, like banks.

Additionally, while the angel investor is taking a bigger risk, the founder is taking a smaller risk, as private funding from angel investments typically don’t have to be paid back if the startup fails.

As angel investors are typically experienced business people with many years of success already behind them, they bring a lot of knowledge to a startup that can boost the speed of growth. As a result, they often invest not only money but also “sweat” equity, in the form of their active involvement, and often request a board member position in the startup.

Disadvantages of working with angel investors

The primary disadvantage of private investments fundraising from angel investors is that founders give up some control of their startup when they take on this type of private investment.

Angel investors are purchasing a stake in the startup and will expect a certain amount of decision making power as the company moves forward. Unlike VCs, angel investors do not usually have a website as such and it’s often difficult to know their investment criteria or portfolio of past investments in advance.

Another disadvantage is that individual angel investors can often not cover the full ticket size of the investment by themselves (like VCs or private equity forms would do) and need to come together in a syndicate. Of course when larger groups of investors are involved, the terms of the deal become more difficult to arrange.

Besides, founders should be aware that having a larger group of smaller investors can dilute their cap table a lot.

Some angels can turn out to be difficult to deal with. They may be ill motivated and in the long run cna even ruin the company. A word of advice is to check the background of the angels about their investments history.

- Venture capitalists

Advantages of working with venture capitalists

Similar to angel investors, private investors such as venture capitalists also come to the table with a lot of business and institutional knowledge.

They’re also well-connected with other businesses that may help a new startup, ner recruits that a startup might want to take on, and connections with other potential investors. Many VCs often run acceleration or business incubation programs that can greatly benefit all startups.

Disadvantages of working with venture capitalists

Also similar to angel investors, part of what venture capitalists want in return for their investment is equity in a startup.

That means that a founder gives up part of their ownership when they bring on venture capital.

Depending on the deal, a VC may even end up with a majority stake, more than 50% ownership, of a startup. That means the founder (or small businesses) essentially lose management control of their startup.

Also, founders should be aware of VC investment cycles, as explained above, and should try to fit within their timing. Asking for an investment at the wrong stage of the VC funds often results in rejection.

Where to find private investors

Finding private investors depends on the type of private investments fundraising a startup is looking for.

We’re not going to go over family and friends, because that’s obvious, and we’re also not going to go over private equity, for all of the reasons outlined above.

But let’s take a look at the other two main types of private investors.

Where to find angel investors

The first place most people can find angel investors is through a founder’s own network. Personal connections are always a good avenue when people ask someone to invest money and trust.

However, not everyone has networks that include very wealthy individuals. In that case, there are a few resources available.

Websites for accessing angel investors:

- National Angel Associations (e.g. Fiban, Estban, Denban etc)

- Angel Investment Network (USA)

- AngelList

- Funding Post

- Gust

- Crunchbase

- Dealroom

- Pitchbook

- Angel investor and pitch events

Where to find venture capitalists

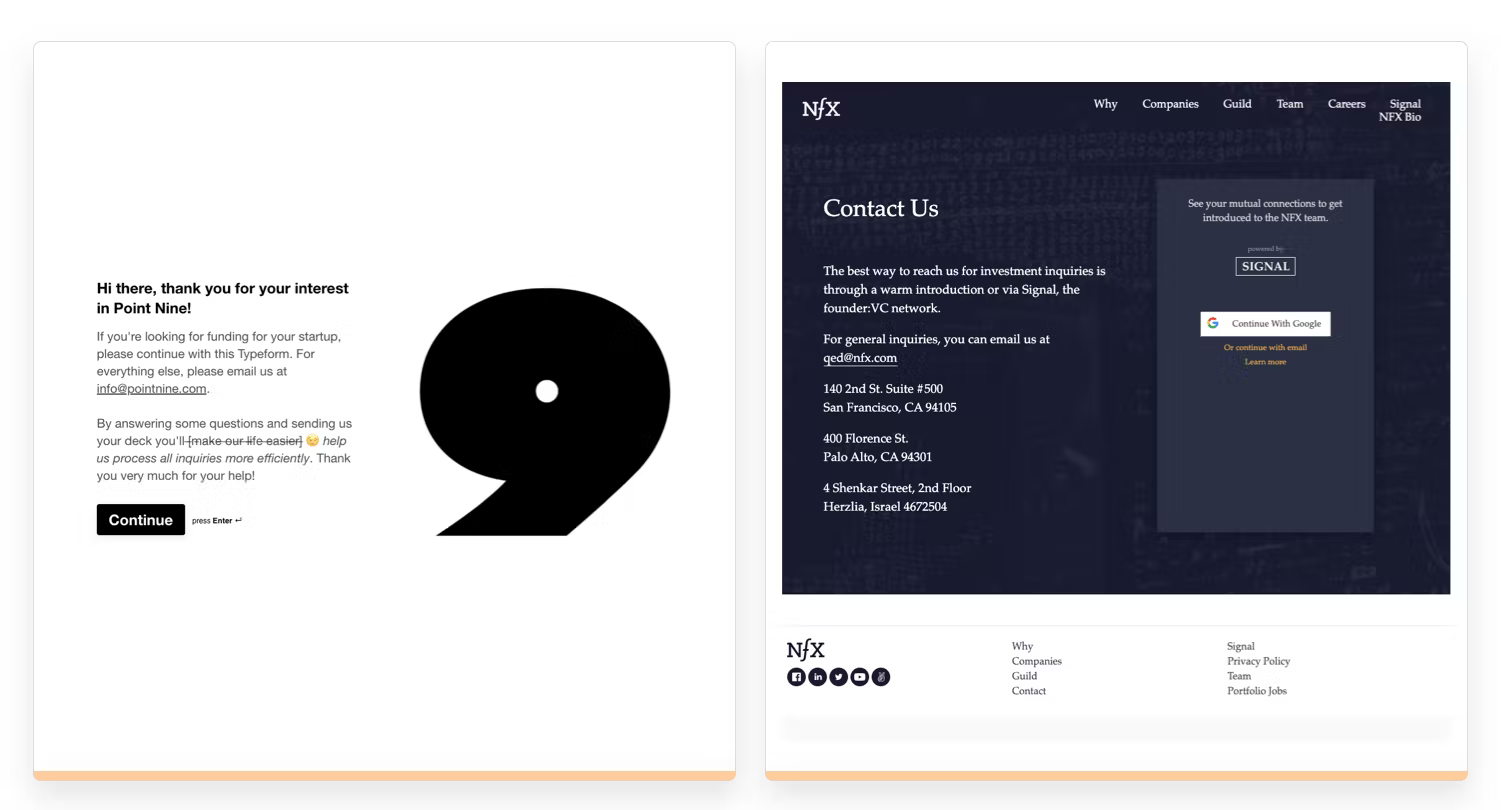

The first step to find venture capital is to make a smart introduction to the venture capital firm the founder wants to meet. Venture capitalists rely heavily on trusted connections to vet deals and some even run their own portal to get referrals, e.g. see the portal Signal below from Point Nine VC.

Founders shouldn’t try to contact as many people as possible; they should try to find venture capital firms that are the best possible fit for their deal.

The more closely aligned the founder is with the needs of the venture firm, the more likely they’ll find venture capital firms willing to write them a check.

Founders should do extensive research both online and through existing networks ahead of time to determine what types of investments a firm makes, as well as whether or not they have any connections with that firm.

Every pitch to a venture capital starts with an introduction to one of the private investors at the firm. It helps to know the exact profile of a venture capitalist to know which level of introduction makes sense. Typically it starts with an introduction to an associate or the fund manager and then founders can work their way up to the full partnership.

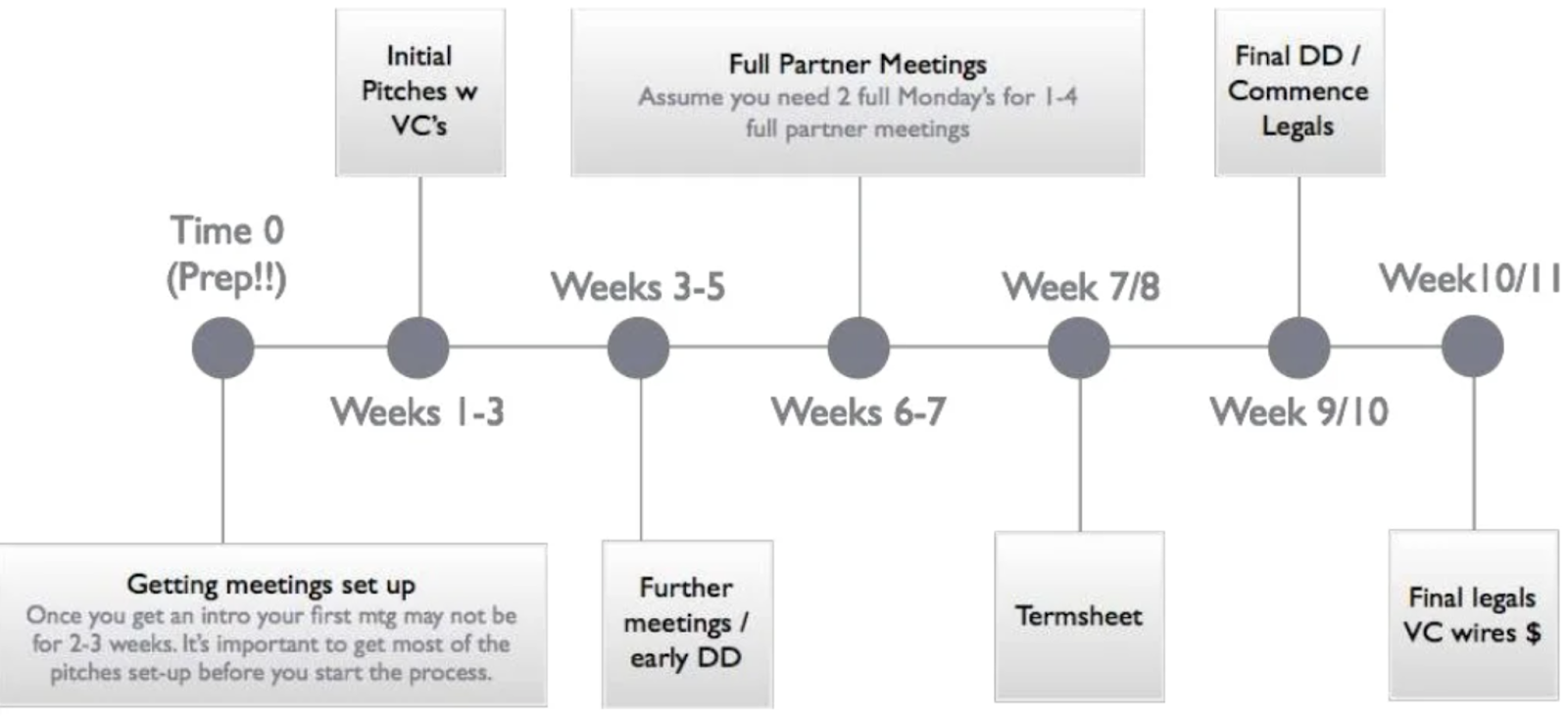

Investment timeline

Founders should bear in mind that it will take 1-18 months as an average to finalize the private investments fundraising round. Angels might take 1-3 months, whereas VCs up to 18 months. VCs might want to “observe” a company for a longer amount of time before investing, so it’s important founders keep the company visible in the different portals and post regular updates like how the company has been doing financially in the last quarter etc.

The typical private investments fundraising timeline looks like this:

Let’s take a look at each of the steps now.

The elevator pitch

The first thing a founder needs to send to an investor is an elevator pitch. The elevator pitch isn’t a sales pitch. It’s a short, well-crafted explanation of the problem a startup solves, how they solve it, and how big of a market there is for that solution and what sets them apart from other competitors.

Founders don’t need to “sell” the product. The opportunity should speak for itself.

So, the following are the essential factors that a private investor looks for before investing in any business:

- Idea or Product: The investors look if the business idea or the product is an original work. They look for it to have distinctive features that sell in the market.

- Business Plan: Investors examine the business plan, including its marketing analysis and product features.

- Management Team: A capable team is an essential element for running a business successfully. Investors look if the management team has the necessary commitment and experience to meet the objective.

- Cash Flow: Investors generally do not invest in a company that barely has turnover or generates a profit. While assessing the firm, they look for earnings before interest, taxes, depreciation, and amortization, known as EBITDA.

- Liquidity: The firm may not pay its debts if it doesn’t have any liquid assets. So, the investors need assurance before investing in a company. They ensure that the company stays within the liquidity agreement.

- Expenses: High expenses can ruin a startup. Investors look to see if a business has an expense control system to keep the unnecessary cost in check.

- Metrics: A business metric is a quantifiable criterion used to track, monitor, and assess a company’s success or failure. There is no one-size-fits-all scale. Different investors use different indicators to measure success, although most often these criteria have monetary value i.e. financial track record etc.

Private investors want to look at these indicators to see how the startup is performing in the market. They would want to know how they could get their profit from the startup when the time arrives.

The first response

When and if the investor responds to an email, the founder will either get a short “no” or a request for more information.

Most angels will request either a one-pager executive summary or a pitch deck. The pitch deck is a 10-15 slides synopsis of the business plan that covers things like the problem, solution, market size, competition, management team and financials. Investors like pitch decks because they force the founder to be brief, and hopefully use visuals instead of an endless list of bullet points. The pitch deck is the founder’s friend and most trusted ally in the investor pitch process.

At this stage, the investor isn’t interested in finding out as much information as possible about the deal at this point. In fact, they are looking to find out as little information about the deal to determine whether or not they want to spend more time with this startup.

It’s not a good idea to overwhelm the investor with every last piece of information ever collected for fear of them “not seeing everything.” They are likely reviewing a dozen other deals at the same time so they couldn’t review everything, even if they wanted to. Founders should simply let them know that more information is available upon request.

The pitch meeting

Once the investor has reviewed the founder’s materials and determined they are interested in meeting with the founder, the next step is to arrange a time for a pitch meeting.

For angel investors especially (but for VCs to some degree as well), the pitch meeting is more about the investor liking the founder as a person than it is just pitching the idea. So, founders should take a little bit of time to try to establish some relationship with the investor even before and after the pitch.

During the pitch, the founder will run through their pitch deck and answer questions. The goal isn’t to get to the end of the pitch deck in 15 minutes or less. The goal should be to find an aspect of the business that the investor actually cares about. If the investor wants to spend 60 minutes talking about the first slide, the founder shouldn’t rush them.

The financials

Of all the documents that a founder is going to be expected to be armed with in the private investments fundraising process, the financials are the most important.

Most investors are going to expect a reasonable five-year projection of the income and expenses of the business.

They’ll want to know how quickly founders will be able to get the startup to break even. They’ll want to know what founders intend to use their money for. And of course, they’ll want to know how founders intend to give it back to them with a healthy return.

Founders should be prepared to provide an income statement, use of proceeds, and breakeven analysis at the very least.

The goal of the private investments fundraising pitch process

The goal of the first few meetings isn’t to “close” the investor, it’s to establish a relationship that will naturally lead to a close.

The investor isn’t someone looking to buy a product.

Founders should be themselves. They should represent the opportunity and their passion for business. That is all they need to convince private investors to do a deal.

The term sheet

A term sheet is the first formal, but non-binding, document between a startup founder and an investor.

A term sheet lays out the terms and conditions for investment. It’s used to negotiate the final terms, which are then written up in a contract.

A good term sheet aligns the interests of the investors and the founders, because that’s better for everyone involved (and the startup) in the long run. A bad term sheet puts investors and founders against each other and that is not good for business growth.

Even getting a term sheet isn’t the same as finalizing the closing legal documents that the term sheet outlines.

This involves a great deal of back and forth between the attorneys from both private investors and founders and can easily take 30 to 60 days to complete if it gets done right. It’s not unusual for this process to go over 90 days, but if it starts dragging over 120 days, the deal runs the risk of falling through.

Due diligence

The last item is kind of a catch-all that we’ll call “due diligence.” When the investor gets more interested in a deal, the next phase of discovery is called due diligence.

During this phase they will dig into all the details of the business, from financials to the details of how the business model works.

This is where all of the research and support the founder has put together will be put to the test. They’re likely going to ask founders to prove how they arrived at the market size they’re going after.

The due diligence possess can be broken down in 3 parts:

- Legal due diligence (regulatory risk, shareholders agreement, cap table, personnel & hiring, invoices, articles of incorporation),

- Technology due diligence (maturity, tech-stack, competitors review, IPR, software/hardware testing),

- Financial due diligence (historic & forecasts, split of proceeds, sales and funnel metrics, CAC ratio, Churn, CLTV).

Founders may get asked to have their early customers talk to the venture capital firm. Assume the investment firm is going to do its best to make sure everything the founder said actually checks out.

It’s only after the due diligence is completed that the investor prepares the shareholder agreement with the founders. That is the last step that seals the deal before writing the check.

Final thoughts

Private investments fundraising and getting an investor on board is difficult for most small business owners. It may be appealing to seek financing wherever it is found, but it is essential to consider the pros and cons of each option before moving forward.

Understanding the investors’ management style, objectives, and goals and following their past performance is crucial before accepting an investment for the startups.

Examine the investors with proper due diligence, as the investors do for startups. Avoid those investors who are keen on gaining control of the business.

Read more about our private investments fundraising services and get in touch to find out how we can help.

About the Author

Marco Torregrossa

Marco is CEO at Euro Freelancers. He spends his time helping companies, executive teams and boards create new portfolios of digital business models and growth strategies leveraging the power of platforms, marketplaces and the gig economy. More about Marco here.

You might also like…

Investor Targeting Is Broken: How to Build an AI Investor Targeting Engine That Converts

Most startup founders don’t have a fundraising problem.They have a targeting problem. You can have a…

Read More

Fundraising Prompts to Save You 10+ Hours a Week

Discover 8 powerful fundraising prompts that help startup founders automate investor outreach, data …

Read More

The EU Funding Shortcut: Leveraging Public Grants to De-Risk Your VC Round

Public grants aren’t just free money—they’re powerful leverage to de-risk your VC round, validate yo…

Read More